Why Bitcoin Crashes and Surges in Minutes Part 3: The Liquidation Machine Behind Extreme Volatility

Bitcoin’s most violent moves are not reactions to news or sentiment. They are the mechanical result of leverage, thin liquidity, and clustered liquidation levels colliding inside a synthetic market structure.

By Edward Miranda, November 2025

Why Bitcoin Futures Invert Their Original Purpose

Before examining how liquidation cascades produce Bitcoin’s most violent price movements, it is necessary to understand what futures markets were originally built to accomplish. Futures did not emerge as engines of speculation. They developed as instruments of stability within real economic systems. Farmers locked in crop prices before harvest to manage uncertainty. Airlines hedged fuel costs to stabilize operations. Manufacturers secured future input prices to plan production with confidence. In each case, futures contracts existed to reduce volatility and anchor economic activity to predictable outcomes.

Bitcoin does not operate within such a framework.

It has no production cycle, no seasonal supply risk, and no industrial consumer dependent upon it as a raw material. There is no operational necessity to lock in a future Bitcoin price in order to support real-world production. Without an underlying economic process to hedge, Bitcoin futures did not evolve as risk-management tools. They evolved almost entirely as vehicles for directional exposure.

This difference fundamentally alters the function of the futures market.

In traditional commodities and financial assets, derivatives tend to stabilize the underlying by transferring risk to those willing to bear it. In Bitcoin, derivatives frequently become the dominant arena of price formation. Instead of absorbing volatility, they often generate it. Instead of reflecting the spot market, they lead it.

This inversion is possible because Bitcoin derivatives are synthetic. Futures contracts, perpetual swaps, and options allow traders to gain exposure without owning real coins. Synthetic Bitcoin can be created instantly and in effectively unlimited quantities. There is no supply constraint at the derivative layer. Leverage allows exposure to expand far beyond the capital committed, and perpetual instruments eliminate the natural reset that expiration once imposed. The result is a parallel market whose scale can exceed the underlying asset it references.

When positioning shifts in this synthetic layer, arbitrage systems enforce alignment across venues in real time. Spot markets are pulled into motion not by changes in long-term ownership or adoption, but by automated mechanisms designed to eliminate price discrepancies. What many assume is organic demand is often the mechanical consequence of derivative repositioning.

This structure explains why Bitcoin’s price can move sharply in the absence of meaningful fundamental change. Long-term holders may remain inactive. No new information may enter the system. Yet price accelerates because exposure, not ownership, has shifted. The short-term chart reflects the state of synthetic positioning rather than the state of the underlying asset.

Once this inversion is understood, Bitcoin’s behavior becomes less mysterious. Volatility is not simply the result of sentiment or immaturity. It is the natural consequence of a market where leverage and synthetic exposure dominate price discovery.

This inversion sets the stage for everything that follows. When a system built on synthetic scale accumulates leverage faster than liquidity can absorb it, instability is not accidental. It is structural.

Leverage as Structural Fragility

Once derivatives become the primary arena of price formation, leverage becomes the defining force shaping market behavior. Leverage expands exposure without expanding capital. A relatively small amount of margin can control a position many times its size. This multiplication effect increases apparent liquidity and volume, but it does so by compressing the system’s tolerance for error.

Leverage does not merely magnify gains and losses. It reduces resilience.

In a lightly leveraged market, price fluctuations are absorbed gradually. Participants can adjust, add collateral, or reassess positions. In a heavily leveraged market, small movements carry disproportionate consequences. Margin buffers are thin. Tolerance bands narrow. The system becomes increasingly sensitive to minor disturbances.

Every leveraged position contains an embedded boundary: a liquidation threshold. This threshold is not psychological. It is mechanical. When price crosses it, the position cannot remain open. The exchange closes it automatically to protect its own balance sheet. There is no discretion, no delay, and no evaluation of broader context. Execution is immediate because the system is designed to eliminate risk the moment it exceeds margin.

This feature transforms leverage from a private choice into a systemic constraint.

As leverage accumulates across the market, liquidation thresholds begin to cluster. Traders rely on similar tools, similar models, and similar risk assumptions. Exposure compresses around common price levels. Beneath a surface that may appear calm, the structure tightens. What looks like stability is often the accumulation of conditional exits waiting to be triggered.

Speed intensifies this fragility. Liquidations occur in milliseconds, executed by automated engines interacting with other automated systems. There is no time for reassessment once thresholds are breached. The system enforces its rules without hesitation. What might have been a manageable adjustment becomes immediate forced action.

High leverage also distorts perception. Extended periods of price stability under heavy leverage are often interpreted as strength. In reality, they frequently signal compression. The longer price remains confined while exposure builds, the more tightly the system is wound. Stability in such conditions is not equilibrium. It is stored energy.

This dynamic explains why periods of low volatility often precede violent moves. Calm conditions encourage larger positions. Funding rates influence crowding. Margin becomes thinner relative to exposure. The market appears quiet, but it is structurally loaded.

At this stage, no dramatic external event is required. A minor price movement is sufficient. Once price reaches the first cluster of liquidation thresholds, fragility becomes visible. The initial disturbance does not need to be large. What matters is the density of leverage surrounding it.

Leverage does not determine direction. It determines consequence. It shapes how the system responds once movement begins. In a market dominated by synthetic exposure, leverage converts ordinary fluctuations into potential inflection points. The market ceases to function as a collection of independent actors and begins to behave as a tightly coupled structure governed by constraint.

This fragility prepares the ground for the next phase. When forced executions begin to interact with one another, small disturbances no longer dissipate. They propagate. The mechanism through which fragility expresses itself is the liquidation cascade.

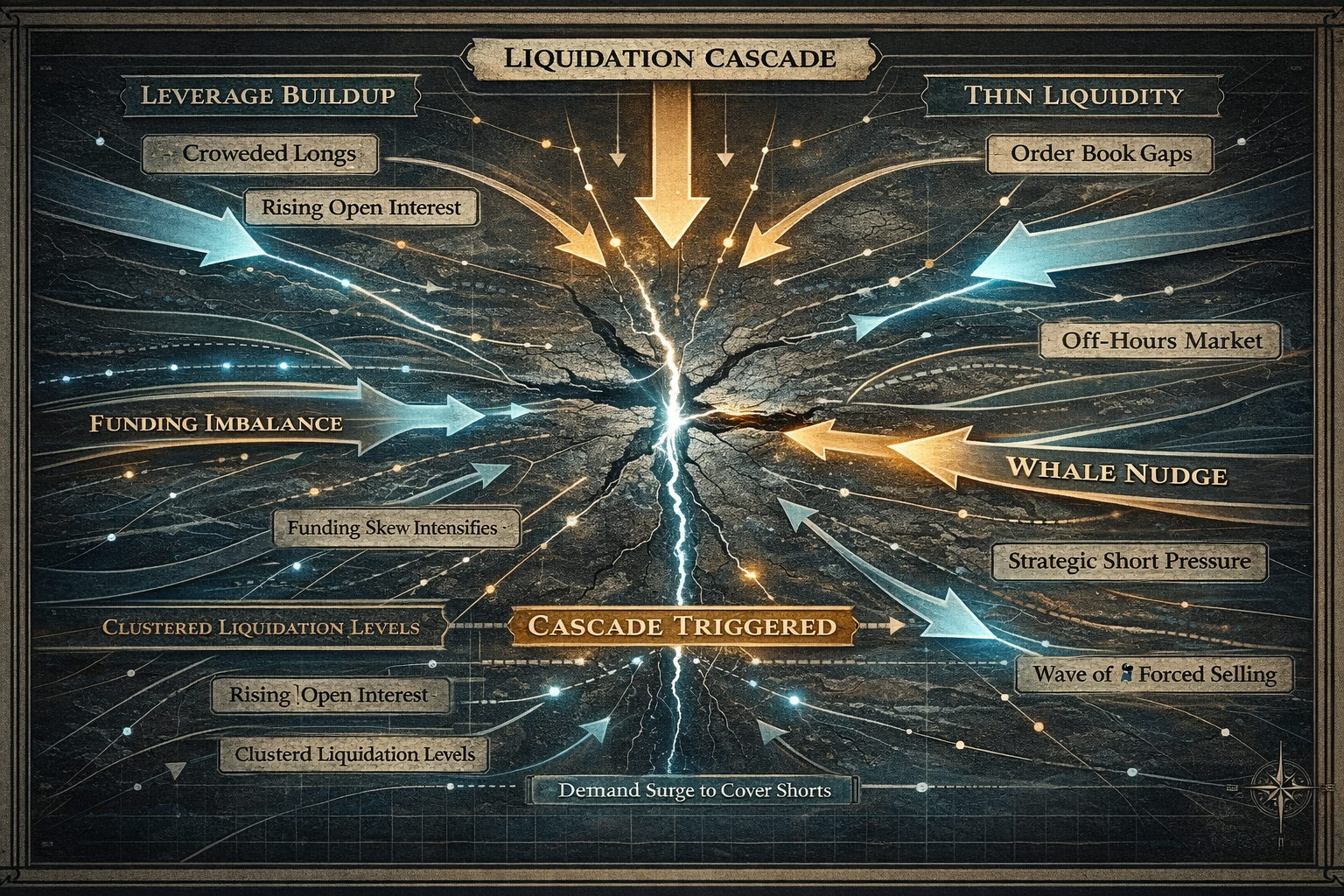

Liquidity Fault Lines, Whales, and Amplification

Liquidation cascades do not unfold in a uniform landscape. They propagate through a market where liquidity is uneven, clustered, and shaped by shared behavior. The severity of a cascade depends not only on leverage, but on the structure of liquidity it encounters.

Liquidity in Bitcoin markets is often described as deep, yet depth is conditional. It concentrates around familiar technical levels, funding imbalances, and psychological anchors. Traders rely on similar models and signals. As a result, positioning tends to compress around common price zones. These zones become structural fault lines within the market.

When price approaches such a region, the system’s ability to absorb forced execution weakens. Beneath what appears to be stable price action lies a dense concentration of stop orders, liquidation thresholds, and leveraged exposure. As long as price remains outside these zones, volatility may remain contained. Once price enters them, amplification becomes likely.

Inside a fault line, each forced trade activates additional constraints. Liquidation thresholds that once appeared distant are breached in rapid succession. The market does not merely continue moving. It accelerates. What might have been a contained adjustment becomes a structural release.

The distinction between a brief cascade and a violent expansion often lies in this relationship between leverage and liquidity. When thresholds are dispersed and liquidity is deep, forced execution can be absorbed. When thresholds are compressed and liquidity is thin, execution propagates through the structure with disproportionate force.

Timing compounds this effect. Liquidity is not constant across hours or conditions. During periods of reduced participation or elevated uncertainty, order books thin. Market makers widen spreads or withdraw capital to manage risk. When forced execution collides with thin liquidity, price gaps emerge. Orders sweep through the book without resistance. Movement becomes discontinuous.

Amplification is further reinforced by arbitrage mechanisms linking synthetic and spot markets. These systems enforce price alignment across venues automatically. When derivatives move sharply, arbitrage engines buy or sell real Bitcoin to close discrepancies. In doing so, they transmit instability outward from the synthetic layer into the spot market.

This transmission is mechanical, not interpretive. Arbitrage systems do not evaluate whether a move is justified. They enforce coherence. As a result, volatility that originates in leveraged derivatives spreads rapidly across exchanges. What began as synthetic repositioning becomes a market-wide event.

Within this environment, large actors exert influence through structure rather than scale. Whales do not need to overwhelm the market with volume. They need only apply sufficient pressure to push price into a vulnerable zone. Once price crosses that boundary, the system responds automatically. Liquidations trigger arbitrage, arbitrage transmits pressure, and amplification unfolds.

The initiating action may be modest. The structural response can be immense.

This dynamic often creates the illusion of coordination or hidden information. Observers search for narratives to explain violent moves. In reality, the outcome was largely predetermined by the configuration of leverage and liquidity already in place. The trigger reveals the structure. It does not create it.

Amplification continues until the system reaches regions of dispersed thresholds and restored liquidity. Leveraged exposure is reduced. Fault lines are crossed. The structure becomes less compressed. Only then does the cascade lose momentum. Stability returns not because sentiment improves, but because fragility has been removed.

Liquidity fault lines, thin participation, arbitrage transmission, and strategic nudges do not create liquidation cascades. They determine how far cascades travel and how much energy they release. They explain why some events register as sharp moves while others reshape the price landscape in minutes.

Once amplification is understood, extreme volatility appears less mysterious. It is the predictable outcome of stress propagating through a tightly coupled synthetic system whose liquidity is uneven and whose enforcement mechanisms operate at machine speed.

What Actually Moves Bitcoin and What It Means for Investors

With the structure now visible, Bitcoin’s behavior becomes far easier to interpret. What once appeared chaotic resolves into a system governed by consistent internal logic. The dramatic movements that dominate headlines are not expressions of mass psychology or sudden shifts in belief. They are the visible outcomes of a synthetic market architecture operating at speed and scale.

The critical distinction is between Bitcoin the asset and Bitcoin the market.

Bitcoin the asset is simple. It is scarce, decentralized, and slow-changing. Its supply is fixed. Its issuance schedule is known. Its long-term value is shaped by adoption, utility, trust, and macroeconomic forces. None of these factors fluctuate minute by minute.

Bitcoin the market is something else entirely. It is synthetic, leveraged, automated, and highly responsive to internal constraints. It is dominated by derivatives rather than real ownership, by machines rather than humans, and by obligation rather than discretion. Short-term price movements reflect the state of this market, not the condition of the underlying asset.

Once this separation is understood, a powerful clarification emerges. Bitcoin’s short-term price is not a verdict on Bitcoin’s future. It is a snapshot of leverage, liquidity, and positioning at a particular moment in time.

Most of the activity that produces dramatic price movement does not involve real Bitcoin changing hands. Long-term holders are often absent from these events altogether. Instead, synthetic exposure expands and contracts, arbitrage systems enforce alignment, and liquidation engines resolve accumulated imbalance. The real asset follows not because it is being reassessed, but because it is mechanically linked to a larger synthetic structure.

This explains why attempts to interpret short-term Bitcoin price action through the lens of sentiment or narrative consistently fail. Sudden drops are assumed to signal loss of confidence. Sudden surges are assumed to reflect adoption or validation. In reality, both are often nothing more than leverage being unwound or repositioned. The market is not expressing belief. It is enforcing constraints.

Understanding this distinction changes how volatility itself is perceived. Volatility is not evidence of instability in Bitcoin as an asset. It is evidence of instability in the structure built around it. Synthetic markets amplify movement because they are designed to do so. They compress risk during calm periods and release it violently when thresholds are breached.

This also reframes the role of large actors. Whales are often assumed to be expressing directional conviction through massive buying or selling. In practice, they operate primarily within the synthetic layer, influencing price by shifting leverage and positioning rather than transferring ownership of real coins. Their influence lies in understanding structure, not in overwhelming markets with volume.

For investors, this understanding offers protection against misinterpretation. It reduces the temptation to react emotionally to sudden moves. It clarifies why extreme volatility can occur in the absence of news and why calm periods can conceal growing instability. It allows price action to be read as structure resolving itself rather than as a referendum on value.

Crucially, none of this diminishes Bitcoin’s long-term prospects or importance. On the contrary, it removes confusion that often obscures serious analysis. The asset remains governed by fundamentals. The path it takes through time is shaped by markets that are imperfect, leveraged, and synthetic.

Synthetic markets control the path, not the destination.

This distinction matters because it restores agency to the observer. Once the mechanics are understood, volatility loses its power to mislead. Price movements can be contextualized rather than dramatized. The noise recedes, and the signal becomes clearer.

Bitcoin’s market will likely remain volatile as long as leverage, automation, and synthetic exposure dominate short-term trading. That volatility is not a flaw to be explained away. It is a feature of the system that has grown around the asset. Recognizing it allows participants to engage with the market more intelligently and with fewer illusions.

In the end, what moves Bitcoin in the short term is not belief, adoption, or fear. It is structure. Leverage accumulates. Liquidity compresses. Constraints are breached. The system corrects itself. What appears violent is simply fast.

This three-part series has traced that structure from its foundations to its consequences. By understanding the synthetic engine, the automated actors, and the liquidation architecture that drive Bitcoin’s price, the market becomes legible. Volatility becomes interpretable. And Bitcoin itself can be evaluated on its merits, separate from the machinery that so often obscures them.