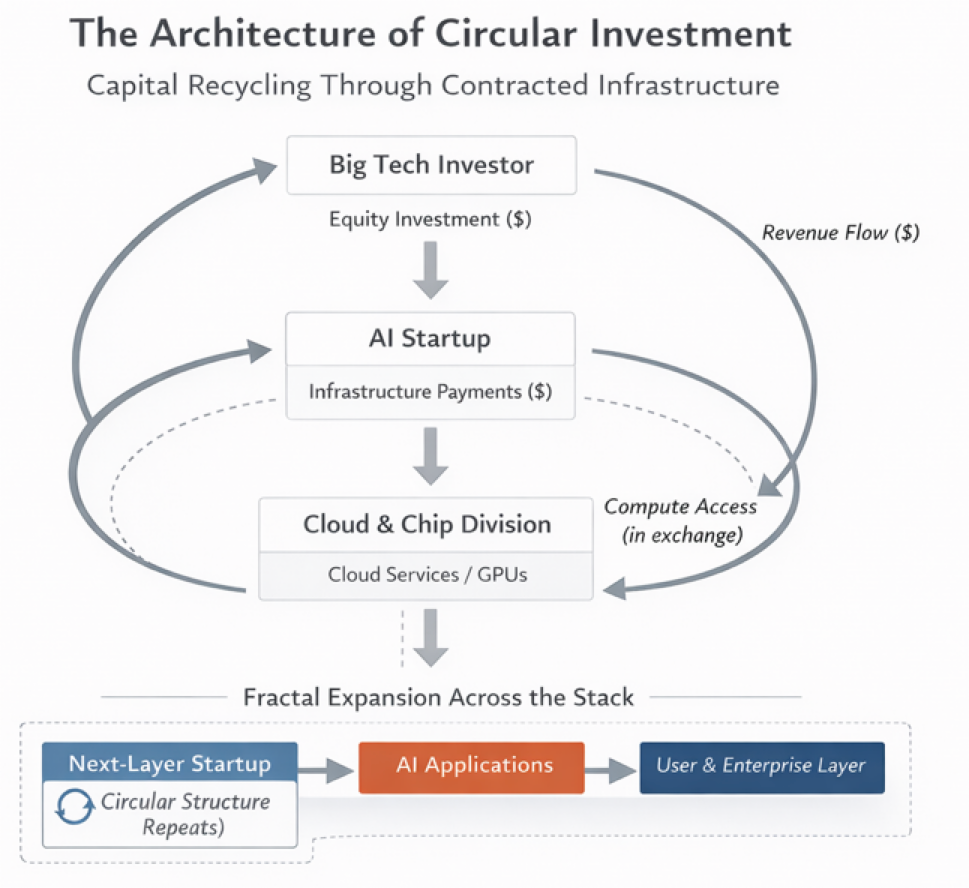

The Architecture of Circular Investment

Big Tech’s AI investments are not isolated bets but part of a circular architecture. Equity, contracted infrastructure revenue, and dependency reinforce one another. This paper examines how capital recycling through cloud and chip agreements reshapes exposure across the AI stack.

By Edward Miranda, February 2026

Abstract

The prevailing narrative surrounding artificial intelligence investment presents a story of bold financial risk-taking by technology giants. This paper argues that the underlying structure is more calculated than it appears. Through an examination of capital flows between major technology companies and AI startups, it demonstrates that a significant portion of headline investment figures is economically offset through pre-negotiated commercial agreements, primarily in the form of long-term cloud computing contracts and chip procurement commitments. These arrangements reduce the effective net exposure associated with equity investments while simultaneously creating operational dependency that secures durable revenue streams for the investor. This recurring architecture, here termed the Circular Investment Structure, represents a sophisticated form of capital recycling and strategic integration that is more coherent, self-reinforcing, and less visible than its public presentation suggests.

1. Introduction

In early 2025, SoftBank led a consortium that announced a $500 billion initiative, branded Stargate, to build AI infrastructure in the United States. Among the participants was Nvidia, which committed $100 billion to the project. Financial markets responded with predictable enthusiasm, and headlines celebrated the commitments as a landmark vote of confidence in artificial intelligence. What received considerably less attention was the accompanying disclosure: OpenAI, the principal beneficiary of the Stargate infrastructure, had simultaneously committed to purchasing tens of billions of dollars worth of Nvidia chips. The investment, in other words, was underwritten in part by a guaranteed commercial contract flowing in the opposite direction.

This pattern is not unique to that arrangement. Across the artificial intelligence investment landscape, a consistent structure emerges: the investing entity is also the primary supplier to the company receiving investment. Amazon has committed $8 billion to Anthropic; Anthropic has designated Amazon Web Services as its primary cloud and training partner. Google has invested over $3 billion in Anthropic while simultaneously signing a cloud computing deal with the company worth tens of billions of dollars. Microsoft has invested over $13 billion in OpenAI while OpenAI has committed to spending $250 billion on Microsoft’s Azure cloud platform.

The purpose of this article is to examine the mechanics, implications, and consequences of what this author terms the Circular Investment Structure: a financial arrangement in which the nominal cost of equity acquisition is substantially recovered through pre-negotiated commercial revenue, leaving the investing party in possession of a valuable equity stake at minimal net outlay.

2. The Mechanics of Circular Investment

The Circular Investment Structure operates through a relatively simple sequence. A large technology company deploys capital into an AI startup in the form of an equity investment. Concurrently, or shortly thereafter, the startup enters into a long-term commercial agreement to purchase cloud computing capacity, semiconductor chips, or related infrastructure services from that same investing entity. These commercial agreements are typically structured across multiple years and at meaningful scale, creating revenue streams that offset a substantial portion of the original capital outlay.

The Amazon–Anthropic relationship illustrates the structure clearly. Amazon committed $8 billion to Anthropic across multiple tranches. In parallel, Anthropic designated Amazon Web Services as its primary cloud and training partner, committing to large-scale infrastructure consumption. Morgan Stanley analysis estimates that AWS revenue from Anthropic could reach $1.28 billion in 2025, rise to nearly $3 billion in 2026, and approach $5.6 billion by 2027. Over a multi-year horizon, cumulative commercial revenue plausibly exceeds the nominal size of the original equity commitment.

This does not imply that revenue is equivalent to profit, nor that the equity stake is without risk. Cloud services carry operating costs, capital expenditures, and margin constraints. The relevant point is more structural. A meaningful portion of the capital initially deployed as equity is economically offset through pre-negotiated commercial revenue streams, thereby reducing the investor’s effective net exposure relative to the headline investment figure. The equity remains on the balance sheet, but the financial risk attached to it is materially mitigated through contractual operating income.

The Google–Anthropic arrangement follows a similar pattern with additional structural nuance. Court disclosures in 2025 indicated that Google holds approximately a 14 percent stake in Anthropic through investments totaling over $3 billion. At the same time, Anthropic entered into a large-scale cloud and hardware partnership granting access to as many as one million of Google’s Tensor Processing Units, a relationship widely estimated to represent tens of billions of dollars in commercial value over time. In effect, Google acquires equity exposure while simultaneously positioning itself to generate infrastructure revenue from the same counterparty. If Anthropic’s valuation appreciates, Google benefits through equity appreciation. If Anthropic scales its operations, Google benefits through infrastructure consumption. The two legs of the arrangement reinforce one another.

Viewed in isolation, each transaction resembles a conventional strategic partnership. Viewed together, they form a recurring architecture: capital moves outward as equity, revenue flows inward as infrastructure consumption, and long-term operational dependency links the two. The economic substance of the arrangement is not that risk disappears, but that it is redistributed and structurally buffered in ways that differ meaningfully from a traditional, standalone equity investment.

A present value framework reinforces the point. If projected AWS revenue from Anthropic over a seven-year horizon is discounted at a rate approximating the weighted average cost of capital for large-capitalization technology firms, typically ranging between 8 and 12 percent under standard corporate finance benchmarks, the net present value of that commercial revenue plausibly approaches or exceeds the nominal size of the original $8 billion investment. Even applying a higher discount rate to reflect execution risk and counterparty uncertainty at the time of commitment, the present value of projected infrastructure revenue remains economically significant relative to the capital deployed.

|

Scenario |

Equity Deployed |

PV of Contracted Infrastructure Revenue |

Net Economic Exposure |

Dependency Created |

|

Traditional VC |

$8B |

$0 |

$8B |

None |

|

Circular Investment |

$8B |

$6–8B (illustrative) |

$0–2B |

High |

It is also important to distinguish between gross revenue and incremental economic benefit. The relevance of the commercial contracts in a circular structure lies not merely in their scale, but in their ability to secure multi-year infrastructure consumption that might otherwise have been uncertain, competed away, or deferred. By converting variable or contestable demand into contracted utilization, these agreements create incremental economic value for the investor relative to a standalone equity position.

The equity position retains full exposure to valuation risk, and the circular structure does not eliminate the possibility of impairment. What it alters is the proportion of capital economically exposed, not the risk characteristics of the equity itself.

The relevant observation is not that the commercial revenue renders the equity position costless, which would be an overstatement, but that it meaningfully reduces the investor’s risk-adjusted net exposure. A conventional venture investor deploying $8 billion into an AI startup bears the full nominal amount at risk from inception. By contrast, an investor operating within a circular structure bears the difference between the capital committed and the present value of contracted commercial revenue, a materially smaller exposure anchored in operating agreements rather than solely in future valuation outcomes.

3. The Valuation Ceiling Problem and How It Is Managed

The Circular Investment Structure contains an internal contradiction that its architects must actively manage. If an investing entity continuously recycles capital into an AI startup while that startup simultaneously returns equivalent sums as commercial revenue, the logical endpoint is troubling: the investor would, over time, acquire an ever-larger equity stake in a company whose valuation it is simultaneously inflating through guaranteed revenue contracts. Carried to its conclusion, the structure would result in the investing entity owning the company it ostensibly invested in, at which point the circularity collapses into simple vertical integration and the fiction of an independent AI competitor disappears entirely.

That this outcome has not materialized is not accidental. Several mechanisms operate in concert to prevent the musical chairs from stopping.

The first is valuation inflation as a dilution tool. As an AI startup raises successive funding rounds at escalating valuations, the percentage ownership held by any single early investor is progressively diluted. Nvidia’s stake in OpenAI, whatever its nominal dollar value, represents a shrinking fraction of an expanding equity pool. The investing entity retains significant value on paper while its control position is diluted by the entry of new capital from pension funds, sovereign wealth funds, and retail participants through secondary markets. The structure thus requires a continuous inflow of external capital to function. New investors absorb the dilution, the early strategic investor’s percentage ownership declines, and the circularity is preserved because no single party approaches majority control.

The second mechanism is the strategic use of non-voting or limited equity structures. Several of the largest AI investments have been structured through instruments that provide economic exposure without corresponding governance rights. Microsoft’s relationship with OpenAI, for instance, involves a capped profit interest rather than conventional equity. This architecture allows the investing entity to recover commercial value through revenue while maintaining the appearance of an arm’s-length commercial relationship. Regulators scrutinizing ownership concentration find the headline ownership figure uninformative; the actual economic relationship is embedded in commercial contracts rather than the cap table.

The third mechanism, and perhaps the most important, is the IPO horizon. The Circular Investment Structure functions optimally as a private market phenomenon. Once an AI company reaches public markets, its ownership structure becomes transparent, its commercial relationships subject to greater disclosure, and its valuation exposed to the discipline of public market pricing. The strategic investors therefore have a strong incentive to extract maximum value before the IPO while simultaneously using the IPO as the terminal event that crystallizes their returns. The retail investor who purchases shares at IPO is, in this reading, the exit liquidity that allows the circular structure to unwind gracefully.

Together these mechanisms ensure that the musical chairs does not stop because the music is continuously extended: new investors enter, valuations rise, ownership concentrations are managed through dilution and structural complexity, and the eventual public offering transfers the residual risk to a market that has been given only partial visibility into the architecture it is being invited to join.

4. The Pipeline Imperative: Manufacturing the Next Cycle

The Circular Investment Structure is not a static arrangement. It is a machine that requires continuous feedstock. When an AI startup reaches public markets, the private market advantages that made the circular structure so profitable, early valuation entry, negotiated commercial lock-in, information asymmetry relative to retail investors, are substantially diminished. The investing entity therefore faces a structural imperative: it must identify, fund, and cultivate the next generation of private AI companies before the current generation exhausts its utility as a circular investment vehicle.

This dynamic has a direct implication for how Big Tech behaves toward its existing portfolio companies. There is a quiet but powerful incentive to accelerate the IPO timelines of OpenAI and Anthropic not because public markets represent the optimal outcome for those companies, but because their graduation to public status frees the investing entities to redirect circular capital toward the next cohort of pre-IPO candidates. The IPO is not the conclusion of the game. It is the mechanism by which one round ends and the next begins.

The pipeline already exists in nascent form. Companies such as xAI, Mistral, Cohere, and Perplexity currently occupy the pre-IPO stage that OpenAI and Anthropic held several years ago. Each is capital-intensive, infrastructure-dependent, and in need of the cloud computing and chip access that only a small number of entities can provide. The terms of their early investment rounds will, in all likelihood, follow the structural template already established: equity acquisition paired with commercial agreements that guarantee revenue return to the investor. The circularity will reconstitute itself around a new set of names.

What sustains the game across cycles is the continuous requirement for large valuations. The circular structure only functions if the equity being acquired is worth acquiring. A startup valued at $50 million does not justify a $3 billion infrastructure commitment. The investing entities therefore have a direct financial interest in ensuring that the AI sector as a whole is perceived as transformative, valuable, and deserving of the extraordinary valuations that justify the circular commitments. The narrative of AI as a generational technological shift is not merely a product of genuine enthusiasm. It is also a structural necessity for the financial architecture that sits beneath it. Inflated valuations are not a side effect of the circular investment game. They are one of its operating requirements.

This creates a feedback loop that is largely invisible to outside observers. Big Tech invests in AI startups, which drives valuations upward, which attracts external capital from pension funds and sovereign wealth funds, which drives valuations higher still, which justifies the next round of circular investment at even greater scale. Each turn of the cycle requires a new cohort of sufficiently large private companies to absorb the capital. The pipeline must be kept full. When it empties, the music stops.

The question of what happens when the pipeline runs dry, when there are no longer sufficient pre-IPO AI companies of adequate scale to absorb circular investment, is one that the current architecture cannot answer. It is the question that participants in the game have the strongest possible incentive not to ask.

5. The Captured Client

The equity arrangement is only half of the value proposition for the investing entity. Equally significant is the operational dependency that commercial agreements create. An AI company that has built its training infrastructure on a particular cloud provider’s hardware does not switch providers easily. The cost of migration, the disruption to model development, and the contractual obligations embedded in multi-year agreements create a structural lock-in that ensures revenue continuity far beyond the initial contract term.

This phenomenon may be understood as the creation of a captured client. Unlike a conventional loan relationship, where the borrower may refinance or switch lenders, the AI startup is operationally bound to its infrastructure provider in ways that transcend financial considerations. Amazon’s $8 billion investment in Anthropic did not merely purchase equity. It purchased a customer relationship whose structural dependency on AWS infrastructure is unlikely to be unwound regardless of market conditions or competitive alternatives.

The historical parallel is instructive. In the early twentieth century, J.P. Morgan and his contemporaries perfected a version of this strategy in the railroad industry. Morgan interests would invest in railroad companies, provide their financing through bond underwriting, manage their banking relationships, and sit on their boards. The railroad was captured at every level of its financial existence. What the present generation of technology companies has achieved is structurally analogous, executed at greater speed and at a scale that Morgan himself could not have imagined. The critical difference is that the railroad had alternative lenders; the AI startup whose models are trained on a proprietary chip architecture has no ready substitute.

6. The Predator Cycle: From Prey to Shark

There is a final transformation that the Circular Investment Structure produces, and it is perhaps its most elegant feature. The AI company that survives the private market gauntlet, absorbs the circular investments of Big Tech, and successfully reaches public markets does not emerge as a liberated independent actor. It emerges as a capitalized entity with a balance sheet, a public currency in the form of tradeable stock, and an acute understanding of the mechanics that were used to capture it. It has watched, from the inside, how circular investment works. It now has both the resources and the institutional knowledge to run the game itself.

The logic is straightforward. A newly public AI company faces two simultaneous pressures. Its public market investors demand growth, and growth in the AI sector is increasingly a function of controlling the infrastructure layer rather than merely consuming it. At the same time, the company has spent years as a captured client, watching its cloud and chip expenditure flow back to its investors as revenue. The rational response is to vertically integrate upward toward infrastructure and simultaneously vertically integrate downward toward the next generation of AI applications and models. Both moves require investment targets. Both moves are best executed through the circular structure the company already understands intimately.

OpenAI’s investment activity in the period leading to and following any prospective IPO illustrates the pattern. The company has moved aggressively into hardware development, pursuing custom chip design to reduce its dependency on Nvidia. It has explored data center ownership. It has made investments in application-layer companies whose primary commercial relationship will be with OpenAI’s own API infrastructure. Each of these moves replicates, at one remove, the structure that Microsoft and others used to capture OpenAI itself. The former prey is building its own captured clients.

Anthropic, similarly, has begun investing in companies that build on its Claude API. The commercial logic is transparent: an equity stake in a company whose primary infrastructure dependency is on your own API is a circular investment in miniature. The invested company’s commercial expenditure flows back to Anthropic as API revenue. The lock-in is structural. The arrangement is mutually beneficial in the short term and asymmetric in the long term, for precisely the reasons that the original Big Tech investments in Anthropic were asymmetric.

What this produces, at the macro level, is a fractal replication of the original structure. Big Tech runs the circular game on AI frontier labs. Frontier labs, once public, run a version of the same game on AI application companies. Application companies, if they reach sufficient scale, will run it on the next layer below them. The structure does not merely repeat across time in successive cycles. It reproduces itself simultaneously across levels of the technology stack, with each layer capturing the one below it through the same combination of equity investment, commercial dependency, and infrastructure lock-in.

The implication for market structure is significant. What appears to be a competitive AI ecosystem, multiple companies at multiple layers pursuing different applications, is, on closer examination, a series of nested circular relationships in which each participant is simultaneously the investor capturing value from below and the captured client generating value for above. Competition exists at the surface. The architecture beneath it is one of layered dependency running in a single direction: upward, toward whoever controls the infrastructure at the top of the stack.

That entity, at present, is a very small number of companies. The circularity, across all its iterations, ultimately flows back to them.

7. The Accounting Fiction: How the Structure Disappears on Paper

The Circular Investment Structure possesses a property that distinguishes it from most forms of financial engineering: it is self-concealing within the standard architecture of corporate financial disclosure. This is not the result of deliberate misrepresentation. It is the consequence of accounting standards that were designed for a world in which investment activity and commercial activity were understood as separate categories of corporate behavior. The circular structure collapses that distinction, and in doing so renders itself invisible to the frameworks built to report it.

When Google invests $3 billion in Anthropic, that commitment is recorded on Google’s balance sheet as a long-term equity investment, subject to periodic fair value assessment. It appears in the investing activities section of the cash flow statement. When Anthropic subsequently purchases tens of billions of dollars of Google Cloud services, those payments appear in Google’s income statement as cloud revenue, contributing to the growth figures that analysts track and shareholders celebrate. The two entries are never presented in proximity to one another. No footnote is required to disclose their structural relationship. No accounting standard compels Google to present the net economic position: equity acquired minus commercial revenue recovered equals actual cost of ownership.

The result is that a transaction which is, in economic substance, a partially self-funding equity acquisition is reported to the public as two entirely unrelated events: a bold strategic investment and strong organic revenue growth. The investment division and the cloud division may even celebrate their respective contributions to shareholder value in the same earnings call, with no obligation to acknowledge that one subsidized the other.

This accounting separation has consequences that extend beyond disclosure. Because the investment and the commercial revenue are recorded in different categories, the circular structure generates what appears to be genuine business momentum across multiple dimensions simultaneously. The equity investment signals strategic confidence. The commercial revenue signals product-market fit and customer demand. Analysts constructing valuation models for Google or Amazon treat the cloud revenue as durable, recurring, and competitively won. None of those characterizations are entirely false. But none of them capture the degree to which the revenue was structurally guaranteed rather than organically earned.

The treatment of the AI startup’s side of the ledger compounds the distortion. Anthropic records its AWS expenditure as an operating cost, which depresses its reported profitability and justifies continued loss-making as an investment in growth. The commercial commitment that generates Google’s and Amazon’s revenue simultaneously provides the AI startup with a narrative of aggressive infrastructure investment that the venture capital market rewards with higher valuations. The spending that flows upward to the infrastructure provider is reframed, on the startup’s own financial statements, as evidence of ambition and scale. The captured client presents its captivity as a competitive advantage.

Under current Generally Accepted Accounting Principles and International Financial Reporting Standards, none of this requires correction. The Financial Accounting Standards Board has not issued guidance specific to circular investment structures, and there is no indication that it is considering doing so. The SEC’s related-party transaction disclosure requirements apply to transactions with affiliates, directors, and major shareholders, but do not compel disclosure of the structural relationship between an equity investment and a subsequent commercial agreement with the same counterparty when the investing entity holds a non-controlling stake.

The practical consequence is that no analyst working from public financial statements alone can reconstruct the true net cost of these equity positions. The information required to do so is distributed across the financial statements of multiple companies, disclosed in different formats, reported on different schedules, and subject to no requirement that it be aggregated or presented in relationship to its counterpart. The opacity is systemic and structural rather than intentional, which makes it considerably more durable than fraud.

8. The Regulatory Gap

Existing antitrust and securities frameworks were not designed with the Circular Investment Structure in mind. Traditional vertical integration doctrine focuses on the acquisition of suppliers or distributors within a single production chain. The structure described here is distinct: the investor is simultaneously a supplier, a commercial partner, and a board-level participant in the governance of a nominal competitor. No existing regulatory category cleanly captures this configuration.

Section 7 of the Clayton Act prohibits acquisitions that may substantially lessen competition, but equity stakes held by strategic investors below majority thresholds have historically received limited scrutiny. The Federal Trade Commission’s 2024 inquiry into AI investment structures acknowledged the gap, but rule making has not followed. In the European Union, the Digital Markets Act addresses gatekeeper dynamics in platform markets but was not drafted to govern the financing relationships between infrastructure providers and model developers.

The argument that these arrangements represent efficient capital allocation is not without merit. AI development requires infrastructure at a scale that few entities can provide. The investing companies have genuine technological capabilities to offer, and the commercial agreements are not concealed. Defenders of the structure would argue that it simply reflects rational specialization: those who own the infrastructure invest in the companies best positioned to use it. That argument, however, presupposes a competitive market for AI infrastructure that does not presently exist. When three companies control the dominant share of cloud computing capacity and the specialized chips required for model training, the efficient capital allocation argument becomes considerably weaker.

9. The Role of the Financial Press

The Circular Investment Structure has flourished in part because financial media has consistently reported headline investment figures without examining their structural context. When a multi-billion-dollar investment is announced, the figure commands immediate attention. The reciprocal commercial commitment, often disclosed in a subordinate clause of the same press release, receives a fraction of the editorial scrutiny.

Several structural factors contribute to this analytical gap. The complexity of these arrangements is genuine; tracing capital flows across investment agreements, commercial contracts, and multi-year revenue projections requires sustained analytical attention that deadline-driven journalism does not readily accommodate. There is also the matter of genuine technological excitement. Artificial intelligence represents a transformative development whose implications are real and consequential. The enthusiasm generated by that transformation creates a narrative environment in which critical financial scrutiny can appear contrarian or ill-informed. The result is a press corps that amplifies investment announcements while underreporting the circular financial architecture that makes those announcements considerably less remarkable than they appear.

10. Implications for Ordinary Investors

The Circular Investment Structure has direct consequences for the retail investor seeking exposure to artificial intelligence. Platforms such as EquityZen now permit accredited investors to purchase pre-IPO stakes in companies like Anthropic, with minimum investments beginning at $5,000. An individual investor purchasing such a stake at Anthropic’s current valuation enters at a price point that reflects years of value creation already captured by early institutional participants.

Google’s initial investment in Anthropic was made when the company was valued at a fraction of its current worth. The structural advantage enjoyed by large technology companies extends beyond financial resources. Their ability to offer cloud infrastructure, hardware access, and commercial partnerships allows them to negotiate equity positions at early valuations while simultaneously guaranteeing their own return through commercial revenue. The retail investor possesses no equivalent leverage and enters the market only after the most significant value appreciation has already occurred.

This is not a novel observation about capital markets. Early-stage equity has always rewarded those with privileged access. What distinguishes the present moment is the scale of the disparity and the sophistication of the mechanisms through which it is maintained. The Circular Investment Structure does not merely concentrate wealth; it does so through financial engineering that presents itself as straightforward investment activity.

11. The Consequences of the Architecture

The Circular Investment Structure is not a neutral financial arrangement. Like any architecture, it produces predictable outcomes for those who operate within it and for those who do not. Those outcomes are worth stating plainly.

For the large technology company that deploys the structure, the consequence is the acquisition of equity in strategically critical companies at a net cost substantially below the headline investment figure, combined with guaranteed revenue streams from clients whose operational dependency makes defection structurally unlikely. The arrangement concentrates both ownership and commercial advantage within a small number of entities that were already dominant before the current AI investment cycle began.

For the AI startup that receives circular investment, the consequence is access to capital, infrastructure, and commercial credibility at the cost of a dependency that compounds over time. The startup that accepts AWS as its primary cloud partner in exchange for Amazon’s equity investment does not merely sign a commercial contract. It accepts a structural relationship that shapes its technology choices, its cost base, its competitive positioning, and its governance in ways that persist long after the initial investment is made.

For the pension funds and sovereign wealth funds that provide the external capital the structure requires to sustain its valuations, the consequence is exposure to a private market whose pricing reflects the circular architecture rather than independent assessment of underlying value. These investors enter after the strategic positions have been established and absorb the dilution that keeps the structure from collapsing into outright ownership.

For the retail investor who accesses pre-IPO stakes through secondary platforms, the consequence is entry at valuations that have already been shaped by years of circular investment activity. The price paid reflects value that was created within the architecture and largely captured by its designers before the retail market was invited to participate.

For the market as a whole, the consequence is a competitive landscape whose surface appearance of diversity, multiple AI companies pursuing different applications across different layers of the technology stack, obscures a deeper uniformity of financial structure. The companies that appear to compete are, in many cases, connected through the same circular investment relationships, dependent on the same infrastructure providers, and subject to the same commercial lock-in dynamics. What looks like competition is, at the level of financial architecture, a series of nested dependencies flowing in a single direction.

For the companies that were never founded because the circular structure raised the cost of entry beyond what any actor outside the existing infrastructure oligopoly could finance, the consequence is absence. Those companies do not appear in any dataset. Their technologies were not developed. Their competitive pressure was never applied. The market that exists is not the market that would have existed without the architecture. That difference is real even though it cannot be measured.

12. Conclusion

This paper has examined a financial architecture that is hiding in plain sight. Its individual components, equity investments, commercial agreements, multi-year cloud contracts, chip procurement obligations, are each disclosed in press releases and regulatory filings. What is not disclosed, because no framework requires it, is the relationship between those components: the fact that they constitute a single coherent structure rather than a series of independent transactions.

That structure operates as follows. A large technology company invests in an AI startup, acquiring equity at an early valuation. The startup simultaneously commits to purchasing cloud computing, chips, or related services from the same investing entity, generating commercial revenue that progressively recovers the cost of the equity position. The startup is operationally bound to its infrastructure provider in ways that make migration costly and contractually constrained. The investing entity therefore holds equity whose effective economic exposure is materially lower than the headline figure implies, in a company whose commercial dependency increases the likelihood of sustained infrastructure revenue over the investment horizon.

The structure does not stop there. It requires continuous external capital to sustain the valuations that justify circular commitments, drawing in pension funds and sovereign wealth funds as passive inflators. It requires a pipeline of successive pre-IPO companies to maintain its private market advantages as earlier cohorts graduate to public markets. It replicates itself as former recipients of circular investment reach public markets and deploy the same mechanics on the layer below them. And it conceals itself within accounting standards that record its two legs, the investment and the returning revenue, as unrelated entries in separate financial statements, with no obligation to present the net position.

The result is a financial architecture that is considerably more sophisticated than its public presentation suggests, considerably more self-sustaining than its participants acknowledge, and considerably less visible to the external observers whose capital and whose markets it depends upon to function.

The architecture exists. It is operating. And it is now, at least in the terms laid out in this paper, understood.

References

Amazon.com, Inc. “Amazon to Invest in Anthropic and Expand Strategic Partnership.” Press release, September 25, 2023. https://www.aboutamazon.com/.

Alphabet Inc. “Google Cloud Expands AI Partnership with Anthropic.” Company announcement, 2025. https://blog.google/.

Damodaran, Aswath. “Cost of Capital by Industry Sector.” NYU Stern School of Business. Updated annually. https://pages.stern.nyu.edu/.

Reuters. “Google Holds Approximately 14 Percent Stake in Anthropic, Court Filing Shows.” March 2025. https://www.reuters.com/.

Reuters. “Morgan Stanley Estimates AWS Revenue from Anthropic Could Reach Multi-Billion Levels.” 2025. https://www.reuters.com/.