The Machines and Whales That Move Bitcoin Part 2: Inside Bitcoin’s Synthetic Engine

Part 2 - Bitcoin’s short-term price is shaped less by sentiment than by synthetic markets and strategic conflict among large participants. When these battles resolve, strategies fail, capital is redistributed, and participants disappear, leaving a thinner market governed by consequences, not intent.

By Edward Miranda, November 2025

How Arbitrage Bots Took Over Bitcoin’s Short-Term Price Discovery

Most people still imagine that Bitcoin’s price is set by buyers and sellers placing manual orders throughout the day. They picture individuals buying a little more during optimism or selling a little during fear. This mental model once reflected reality in Bitcoin’s early years, but it no longer describes how the market operates. Today, almost every short-term movement on the chart is shaped by automated systems reacting to price discrepancies across markets rather than by discretionary human decisions.

These systems are arbitrage bots, and they have become the true engines of Bitcoin’s short-term price discovery.

For clarity, when referring to synthetic markets, this essay means derivatives such as futures, perpetual swaps, and options that reference Bitcoin’s price without requiring ownership of real coins. These instruments now dominate Bitcoin’s trading activity.

Bots Do Not Care About Fundamentals

Arbitrage bots do not evaluate Bitcoin’s technology. They do not assess adoption, monetary policy, or long-term narratives. Their function is narrow and mechanical. They search for price differences between related markets and eliminate those differences as quickly as possible. Any deviation between prices represents risk-free or near risk-free opportunity, and that opportunity is removed almost instantly.

These systems operate simultaneously across spot exchanges, futures contracts, perpetual swaps, and global liquidity feeds. When prices diverge even slightly, the response is automatic. No conviction is involved. No outlook is considered. The bots simply execute until alignment is restored.

This distinction matters because it separates price movement from meaning. In modern Bitcoin markets, movement often reflects the enforcement of mathematical relationships rather than a change in belief about the asset itself.

Bots Enforce Alignment Between Spot and Futures

Whenever a gap appears between spot and futures prices, arbitrage bots respond immediately. If futures trade below spot, bots sell spot and buy futures. If futures trade above spot, bots buy spot and sell futures. These actions occur continuously and at scale.

The important point is that real Bitcoin is traded on spot markets not because someone decided to accumulate or distribute, but because a synthetic discrepancy demanded correction. Spot becomes the balancing mechanism for derivative imbalances.

This process effectively binds the real and synthetic markets together. Futures may move first, but spot is compelled to follow. The direction of causality is no longer intuitive. In many cases, price movement begins where leverage is cheapest and fastest, then propagates outward through arbitrage.

Why Bots Follow Synthetic Markets First

Synthetic markets dominate because of scale. Trading volume in futures and perpetual swaps routinely exceeds spot volume by multiples. Leverage allows large nominal exposure with relatively little capital, making derivatives the preferred arena for short-term positioning.

Because synthetic markets are larger and more active, they generate price discrepancies more frequently. Arbitrage bots therefore focus their attention where misalignments are most likely to appear. When synthetic prices shift, bots must act, and their actions require trading real Bitcoin on spot exchanges.

This is how synthetic markets end up controlling real price behavior. Spot is not ignored. It is used.

Why Bitcoin Often Moves Before the News

This structure explains why Bitcoin often moves before any public news appears. The assumption is usually insider knowledge or coordinated action. In reality, synthetic markets may simply shift first due to positioning, funding dynamics, or changes in leverage.

When synthetic prices move, arbitrage systems respond instantly. Spot prices adjust as a consequence, not a cause. Observers watching the chart see sudden movement and search for an explanation, often finding one after the fact. Yet nothing in the external world may have changed at all.

The movement was structural, not informational.

Human Influence Has Nearly Disappeared

In this environment, human traders have little influence on short-term price direction. A retail order of a few thousand dollars is insignificant compared to the size and speed of synthetic flows. Even large discretionary traders rarely affect price unless their activity disrupts derivative alignment.

Markets that once reflected collective psychology now behave more like automated control systems. Humans still participate, but their actions are filtered, amplified, or neutralized by machines operating at millisecond speeds.

The chart no longer records emotion directly. It records enforcement.

Synthetic Liquidity Shapes Support and Resistance

This dynamic also reshapes how support and resistance form. Traditional analysis assumes these levels represent areas where buyers and sellers naturally congregate. Increasingly, they reflect concentrations of synthetic exposure.

Funding rates, open interest, liquidation thresholds, and options positioning create zones where mechanical reactions are likely. When price approaches these areas, behavior accelerates not because participants agree on value, but because systems are programmed to respond.

When such a level breaks, the move often appears sudden and violent. The reason is structural. Synthetic positions unwind, leverage collapses, and arbitrage systems amplify the adjustment.

Every Candle Reflects Automated Forces

Understanding this structure changes how price action should be interpreted. Rapid moves do not necessarily signal enthusiasm or panic. They may reflect derivative repositioning followed by arbitrage execution.

Humans cannot trade at this speed. Bots can, and they do. The pace itself is diagnostic. When movement is too fast to reflect decision-making, it almost certainly did not originate from one.

The True Engine of Bitcoin’s Short-Term Price

The conclusion is straightforward. Bitcoin’s short-term price is governed by the interaction between synthetic markets and arbitrage systems. Spot markets respond because they must. The crowd no longer leads. It follows.

Once this is understood, much of Bitcoin’s daily volatility becomes intelligible. What appears chaotic is often the visible output of invisible structure.

This Does Not Diminish Bitcoin, It Explains It

Recognizing this mechanism does not undermine Bitcoin’s legitimacy. The asset remains scarce, secure, and decentralized. Long-term value is still driven by adoption, trust, and monetary properties.

What has changed is the pathway between fundamentals and price. In the short term, that pathway runs through synthetic liquidity and automated enforcement. Seeing this clearly replaces confusion with clarity.

Why Whales Can Still Move the Market Without Selling Real Bitcoin

Many assume whales influence price only by selling large amounts of real Bitcoin. In today’s market, that assumption is outdated. Whales can exert enormous influence through synthetic exposure alone. Power comes from pressure, not possession.

A whale can open large futures or perpetual positions using leverage. No real coins are required. If the resulting synthetic movement is large enough, arbitrage systems will trade spot Bitcoin on the whale’s behalf by enforcing price alignment.

The whale never touches a coin. The market still moves.

Liquidity Pockets and Structural Weakness

Whales understand that liquidity is unevenly distributed. Some areas contain dense clusters of stop losses, liquidation levels, and over-leveraged positions. These zones are fragile.

A whale does not need to overpower the entire market. They only need to push price into one of these structural weak points. Once reached, forced unwinds take over. Liquidations cascade. Arbitrage accelerates the move. The whale initiates pressure. The system completes the motion.

Leverage Amplifies Small Actions

When open interest is high, the market becomes unstable. A relatively modest synthetic position can trigger disproportionate consequences. Leverage magnifies imbalance.

This is why large price moves often coincide with little on-chain activity. The action occurred in the synthetic layer. Real Bitcoin was merely the balancing instrument.

Options, Timing, and Market Sensitivity

Options markets add another layer. As contracts approach expiration, price sensitivity increases near key levels. Small synthetic adjustments can force market makers to hedge, requiring spot buying or selling.

Timing also matters. During periods of thin liquidity, synthetic markets are easier to move. Gaps open faster. Arbitrage responses become more aggressive. Strategic positioning during these windows can have outsized effects.

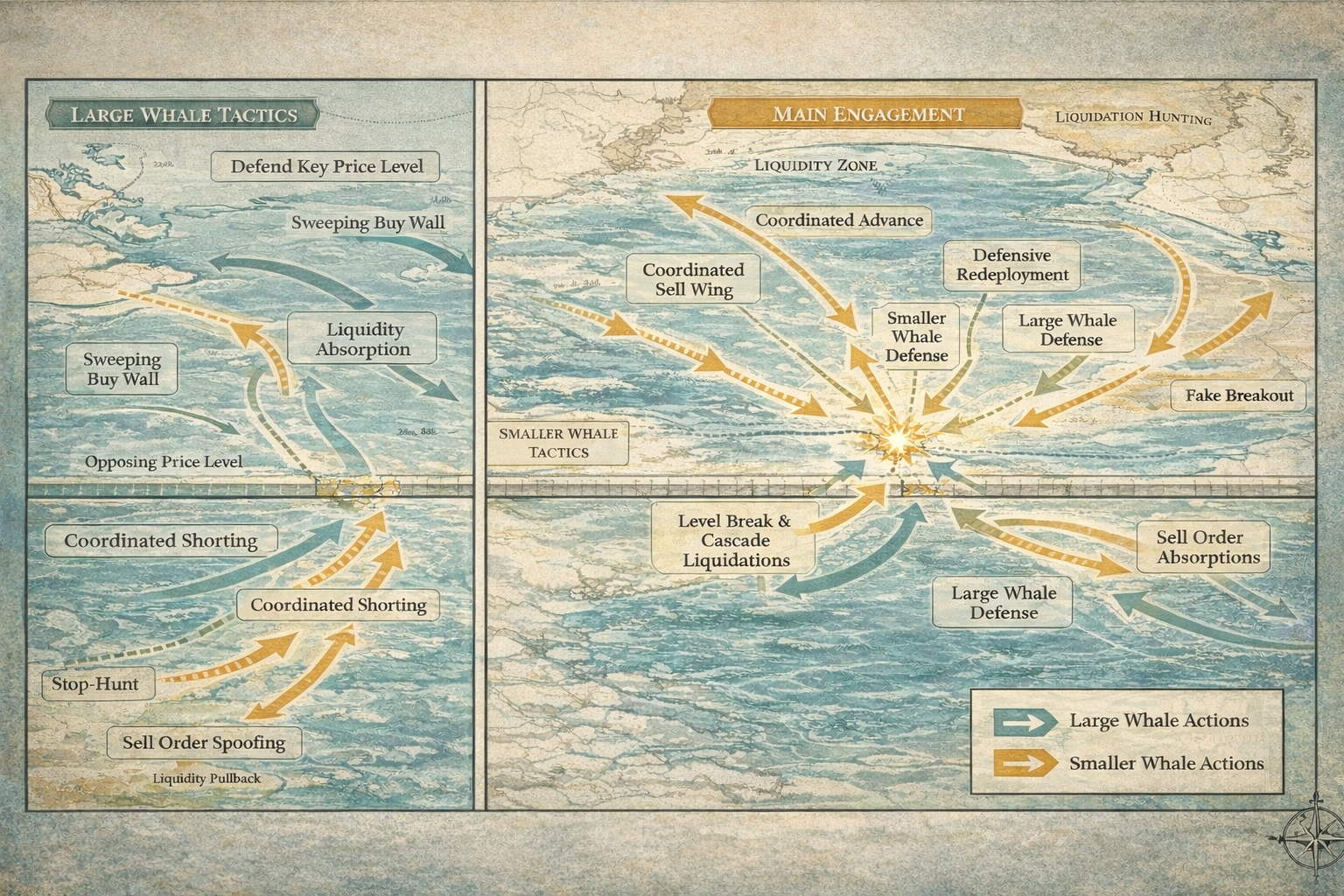

The Whales’ War

Traders sometimes describe the ongoing competition between large synthetic market participants as the “Whales’ War.” This informal term refers to the continuous struggle among whales, funds, and automated trading systems as they apply pressure to Bitcoin’s synthetic markets in opposing directions. The term is not metaphorical exaggeration. It reflects a real structural conflict embedded in modern market mechanics.

Whales rarely act in isolation. Every significant synthetic position exists within a landscape of other large positions, each with its own leverage profile, liquidation thresholds, and time sensitivity. When one whale applies synthetic pressure to drive futures prices lower, another may be forced to defend a critical level because a breach would threaten their own exposure. Price movement becomes less about conviction and more about survival.

These confrontations occur almost entirely in futures and perpetual swaps markets, where whales can deploy massive nominal positions without touching real Bitcoin. Ownership is irrelevant in this arena. What matters is influence. The objective is not to express a view on Bitcoin’s value, but to force price into zones where opposing positions unravel.

Arbitrage bots serve as the translation layer in these conflicts. When a whale succeeds in pushing synthetic markets into a vulnerable zone, bots immediately execute the spot-side trades required to enforce alignment. Real buying or selling appears on exchanges even though the initiating whale never interacted with real coins. The synthetic battle produces real consequences.

What appears on the chart as erratic or chaotic price action is often the surface-level echo of these hidden engagements. One whale pushes. Another whale defends. Liquidity pockets become front lines. Liquidation levels become targets. The market may stall unexpectedly, reverse sharply, or break violently through key levels not because of retail sentiment, but because the largest participants are actively contesting control beneath the surface.

Weapons of the Whales’ War

Whales do not fight each other with traditional discretionary buy and sell orders. Their conflicts unfold through a set of tactics designed to exploit market structure, leverage, and forced behavior. These tactics are often described in weapon-like terms because they are aimed not at persuasion, but at compulsion.

One common tactic is stop hunting, where a whale pushes price into areas dense with stop-loss orders placed by other traders and funds. Triggering these stops unleashes forced buying or selling, allowing the attacking whale to gain momentum without committing significant additional capital. The market does the work once the threshold is crossed.

Another tactic is liquidation hunting, which targets zones where leveraged participants have thin margin buffers. Driving price toward these liquidation levels forces automatic position closures that cascade rapidly. The resulting move is often far larger than the initial synthetic pressure applied, as leverage amplifies the effect.

Whales also deploy synthetic buy walls and sell walls in derivatives markets. These walls are rarely intended to be filled. Their purpose is to influence positioning and behavior. Other large participants must decide whether the wall represents genuine intent, a temporary defense, or a deliberate trap. These structures shape the battlefield by altering risk perception rather than by executing trades.

During periods of thin liquidity, whales may initiate timing attacks, placing large synthetic orders when order books are shallow and market depth is weak. In these conditions, relatively modest pressure can produce exaggerated movement, pushing price rapidly into sensitive areas where opposing whales are forced to react. Timing becomes a force multiplier.

Some whales engage in level defense, aggressively opening or adjusting synthetic positions to prevent price from breaching zones that would threaten their own liquidation thresholds or options exposure. These defenses can temporarily stabilize price, creating the appearance of strong support or resistance until the structural balance shifts.

These tactics constitute the practical weapons of the Whales’ War. None of them require selling real Bitcoin. All of them operate entirely within the synthetic layer, where leverage, liquidity distribution, and automated responses can be weaponized. What appears to be a sudden breakout or breakdown on the chart is often the direct result of these strategic engagements between large players competing for control of the market’s next move.

Why Whale Selling Rumors Are Usually Wrong

This framework explains why rumors of whale selling are frequently false. On-chain data often confirms that major holders did not move their coins during sharp declines. The selling was synthetic. The consequences were real.

Seeing the Market Clearly

Once this structure is understood, Bitcoin’s behavior becomes less mysterious. Ownership matters long term. Influence matters short term. Synthetic force moves price. Arbitrage enforces it. Bitcoin itself remains real. The market around it is increasingly synthetic.

In Part 3, we will examine how liquidation cascades transform small synthetic imbalances into the extreme volatility that defines the current Bitcoin’s markets.